17 November 2017

The Futures of Europe, Negotiable and Non-Negotiable

In commemoration of the sixtieth anniversary of the Treaty of Rome, the European Commission has launched a White Paper on the Future of Europe to frame a conversation about the European Union’s post-Brexit possibilities.

The White Paper celebrates the European Union’s achievements to date (and rightly so) before offering five overlapping scenarios for the “state of the union” in 2025:

(1) Carrying on;

(2) Nothing but the single market;

(3) Those who want more do more;

(4) Doing less more efficiently;

(5) Doing much more together.

All five scenarios represent positive visions for the future, though obviously the Commission is most enthusiastic about the last scenario. It should be equally obvious that neither this full-integration scenario nor the scaled-back EU of the second scenario could be accomplished by 2025, since both would require renegotiations of EU treaties. Nor could the third and fourth scenarios be realistically implemented in such a short time frame, given the broad cross-national social consensuses they would require. The only realistic scenario for 2025 is “Carrying on” with 27 member states instead of 28.

But over a longer time frame, significant institutional change is possible, and even inevitable. Looking out toward the 100th anniversary of the Treaty of Rome in 2057 gives much greater scope for imagining achievable scenarios for Europe’s future. Economic and demographic trends are already in motion which will determine the macro-level socio-economic and socio-political environment of mid-century Europe. Fashionable prognostications for the middle future focus on cataclysmic changes like the rise of robotics, the end of work, or the Islamisation of Europe. These are possible, but perhaps a bit fantastical. Data-driven social science, however, can deliver much more certain predictions, especially concerning medium-term socio-economic and socio-political change.Other trends already in motion are perhaps less dramatic but more certain, because they are driven by slow-changing socio-economic forces that are already at work and take decades to change. Three of the most important are the slowdown in international economic integration, the rise of Turkey as an economic power relative to Russia on Europe’s eastern borders, and the massive demographic expansion of Africa. These trends do not necessarily make any one strategy for the future more attractive than another, but they are factors that should be taken into account in any discussion of the EU’s policy alternatives. To be viable, any scenario for the future of the European Union must include a plan for accommodating (or countering) these three macro-trends.

EUROPEAN INTEGRATION AND CONVERGENCE

The European Union is one of the world’s three advanced economic regions (along with North America and East Asia), with an EU-wide GDP per capita of €29,000 in 2016. Though this is substantially (26%) less than the GDP per capita of the comparable demographic and economic area of NAFTA, it is more than three times the world average of about €8,600. At a long-term economic growth rate of just under 1.5% per year, the EU’s GDP per capita would be expected to double roughly every 50 years. By the 100th anniversary of the Treaty of Rome in 2057, the EU’s GDP per capita should be around 75–80% higher than it is now, or around €52,000 in today’s terms.

If all EU countries grow together at the same rate, this implies that by mid-century a lower-middle-income member state like Poland would grow to a level of GDP per capita roughly equivalent to that enjoyed by Germany today, while today’s poorest member state (Bulgaria) would still lag behind today’s EU average GDP per capita. This assumes no convergence in incomes per capita among member states. A major unrecognised opportunity to raise the overall growth rate of the EU is the rapid development of the EU’s poorer member states. These countries should have the opportunity to take advantage of their relative backwardness to “catch up” with the more advanced EU countries that are closer to the world’s technological frontier.

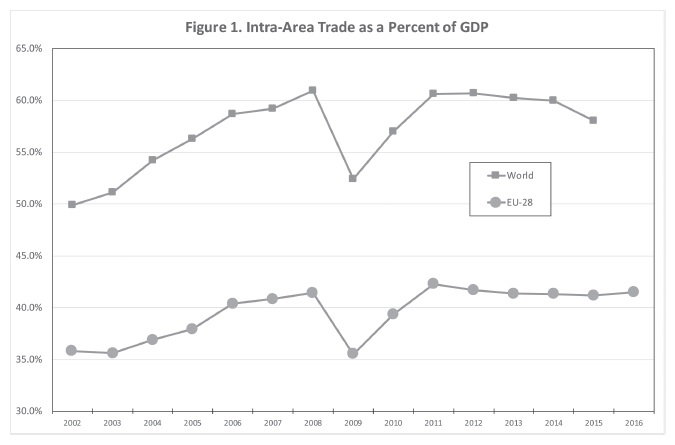

Unfortunately the prospects for catch-up via trade integration seem to be diminishing. Whatever the rhetoric of “ever closer union”, the reality is that trade integration has stalled in the European Union – and globally. Figure 1 charts the trajectory of trade (imports + exports) as a percentage of GDP for the EU and for the world as a whole. The EU figures represent intra-EU trade only (i.e., trade among member states). The graph starts in 2002 because that is the first year for which intra-EU trade data are readily available, but the global level of trade as a percentage of GDP rose consistently from less than 25% in the mid-1960s to a high of 61% in 2007.

Both for the EU and for the world as a whole, the global financial crisis (GFC) of 2007–2009 represented a clear inflection point. Trade was rising rapidly before the crisis, fell dramatically during it, and recovered to its 2007 level afterwards – but has remained stuck at roughly the 2007 level since the end of the crisis. Globalisation as an on-going process of global economic integration seems to have played itself out. We now live in a world of “full” or “mature” globalisation in which market forces are no longer pushing forward higher levels of international trade. China’s One Belt, One Road (1B1R) initiative might be seen in this light. The small increases in intra-Eurasian trade promoted by 1B1R have only been achieved through high levels of government initiative. Market forces alone are not sufficient to promote higher levels of China–EU trade.

The stagnation in intra-EU trade will likely make it more difficult for the poorer countries of the EU to catch up with the richer ones. An EU that grows in lock- step within its current economic structure will reproduce today’s inequalities, but even worse, it will forgo the potential “free” gains from economic convergence that could result from poorer countries advancing toward the economic frontier. Detailed analysis of this problem would require extensive economic modelling, but an indicative analysis suggests that during and after the GFC labour mobility may have taken the place of trade integration: instead of exporting jobs to poorer member states, leading member states are importing people. This process may be functional for the EU as a whole, but it is not conducive to industrial upgrading strategies for the poorer member states.

Though the EU and its member states are limited in their ability to shape the trajectory of global economic integration, they do have policy tools that could be used either to promote or retard further economic integration within the EU itself. Personal mobility is now almost unfettered for most of the EU and EFTA, but substantial institutional and infrastructural restraints still limit full trade integration. Infrastructural barriers still reinforce the old East–West division of the continent after more than a quarter of a century of integration. The institutional restraints on East–West trade are probably larger, especially for trade in services, which constitutes 75% of EU GDP. Integration will not increase automatically in the future. It will take dedicated policies (and spending) to make it happen.

EASTERN THREATS AND PARTNERSHIPS

Specific scenarios for future security threats to the EU are difficult if not impossible to outline on a timescale of forty years, but demographic and economic trends can provide some basic parameters within which such threats could emerge. The EU’s eastern neighbours are all undergoing rapid change, but the EU itself is very stable, both economically and demographically. The EU’s total population is expected to grow by about 4% by the middle of the century, after which it will begin to shrink. It can thus be thought of as a fixed benchmark against which to judge its neighbours.

While the EU population will grow slightly, the Russian population will continue to fall. The UNPD estimates that Russia’s population will fall by 7.3% by mid-century, by which point the current EU-27 will have a three and a half times bigger population than Russia. Likely expansion of the EU into the western Balkans could raise the EU’s demographic advantage to four times larger. The Future of Europe White Paper takes at face value the UK Ministry of Defence forecast that Russia’s military expenditures will rise nearly threefold by mid-century, but this is extremely unlikely.

Russia’s military expenditures are already 60% higher than those of the United States on a percentage of GDP basis (5.3%) and cannot rise much higher without forcing an economic collapse of the kind that broke up the Soviet Union. The Russian economy is highly dependent on hydrocarbons and is unlikely to grow faster than the EU economy in a rapidly de-carbonising world. Today the EU-27 already outspends Russia by a 2–1 margin, and were EU countries to spend even 2% of GDP on defence, they would collectively outspend Russia by a 4–1 margin by mid-century. With the exception of its nuclear arsenal, Russia does not pose a serious long-term threat to a united EU or an EU united within NATO.

Turkey is likely to grow to rival Russia by mid-century. It is already slightly richer than Russia on a per-capita basis; its economy is more concentrated in growing sectors than is Russia’s, and its population is projected to grow from 55% of today’s Russia to 72% of Russia’s at mid-century. Thus by mid-century it is very likely that Turkey’s economy will grow in size from two thirds of Russia’s total GDP to equal Russia’s GDP. Depending on Turkey’s political evolution over the next forty years, it is thus entirely possible that Turkey will replace Russia as the EU’s biggest external security threat.

Turkey is, of course, a NATO member. But NATO itself will become less relevant for Europe’s defence as the threat posed by Russia recedes. This may seem counter-intuitive in the 2010s in light of Russia’s increasing belligerence. But just as today’s Russia is a much less menacing enemy than was the Soviet Union of 1957, the Russia of 2057 will be a much less menacing enemy than the Russia of today – whatever its political leanings, which can hardly become more anti-Western between now and then. A belligerent Turkey, by contrast, would be much more difficult to confront precisely because it is within NATO, making it very difficult for Europeans to use NATO as a tool to contain Turkey. It is not preordained that mid-century Turkey will be hostile to the EU, but of all the EU’s neighbours it is the one country that will have the greatest capacity to threaten the EU, should relations turn sour.

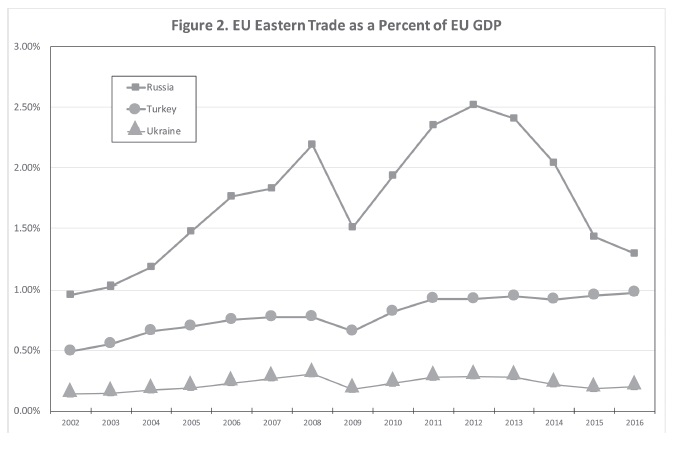

As shown in Figure 2, Russia is a more important trading partner for the EU than Turkey is, but Russia’s EU trade is dominated by hydrocarbons. European hydrocarbon use is in long-term decline, and Russia is poorly integrated into European value chains. Continuing western sanctions on Russia are likely to exacerbate these trends, perhaps over a period of decades. Turkey, by contrast, has a diversified economy that is becoming steadily more integrated with that of the EU. In fact, Turkey and Russia are already roughly equal as EU export markets. Given the higher expected economic and population growth rates in Turkey over the next several decades, Turkey will almost certainly become the EU’s most important Eastern trading partner. Unlike Russia, it will have a strategic leverage over the EU’s energy supplies. With a very different economic profile from Russia, Turkey offers different opportunities for engagement than Russia does.

Although Ukraine has a much smaller economy than either Russia or Turkey and has a rapidly declining population of 45 million (expected to decline to 36 million by mid-century), there might be strategic advantages in helping Ukraine integrate more closely into the EU economy. Current levels of EU–Ukraine trade are very low, less than €30 billion a year. While greater EU integration with Ukraine would not have any substantial impact on Europe’s future, it could have a major impact on that of Ukraine. Long-term strategies for the future of the EU must take into account the shift in potential threats and partnerships from Russia to Turkey, but they might also explore the opportunity to dramatically increase engagement with Ukraine.

AFRICA: THE NEW DEMOGRAPHIC GIANT

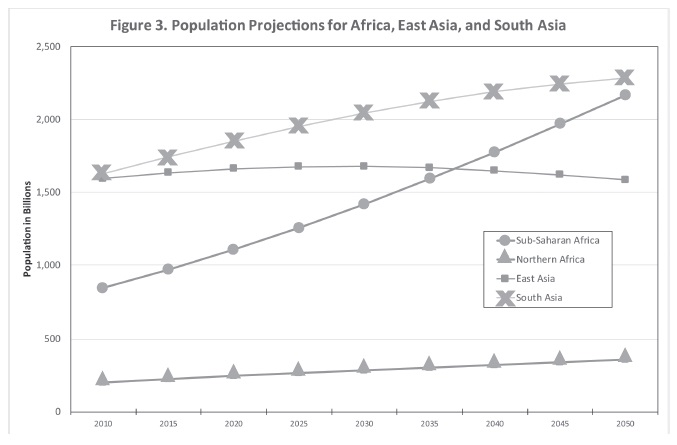

Whereas the EU’s eastern neighbours are expected to lose population over the course of the 21st century, and the EU’s south-eastern neighbour, Turkey, is expected to grow substantially, the EU’s southern neighbours across the Mediterranean Sea in Africa will almost certainly grow by leaps and bounds. The six countries of North Africa – the five Mediterranean countries plus Sudan – are expected to grow by 60% between now and 2050. Seen in isolation, that kind of growth might trigger a demographic crisis, but it is mild compared to the expected growth in sub-Saharan Africa. The 48 countries of sub-Saharan Africa, taken together, are expected to grow by nearly 125% by mid-century, i.e. from a total population of 970 million today to more than 2 billion in 2050.

There are currently around half a million citizens of sub-Saharan African countries living in Italy (exact data are unavailable), constituting a very visible minority approaching 1% of the population. In contrast to the massive wave of immigrants and refugees fleeing the civil war in Syria, most irregular African migrants to Italy come from very poor countries and have low levels of formal education. This phenomenon reflects the economic profile of the continent as a whole, which is much less developed than the Middle East. Moreover, whereas the bleak conditions that have driven Syrians and other Middle Easterners to seek refuge in the EU are transitory when seen from a 40-year perspective, the desperate conditions facing Africans living in refugee settlements and urban slums are structural. Middle Eastern conflicts may in the future spark episodic humanitarian crises, but sub- Saharan Africa suffers from a chronic humanitarian crisis which is likely to worsen over time.

The current African refugee influx to Italy represents the leading edge of what is almost certain to become a much larger flow. As Figure 3 illustrates, sub-Saharan Africa will overtake East Asia and close in on South Asia as the most populous sub-region of the world. By 2050, Africa as a whole will already have more people than South Asia. Nigeria alone is expected to have a population superior to 400 million people, nearly as many as the EU-27. Moreover, there are no signs that Africa’s population growth will end at that point, though it may slow down if family planning norms change over the next two generations.

Extreme population growth in Africa (especially sub-Saharan Africa) is almost certain to interact with climate change to exacerbate water insecurity and other causes of civil unrest in many African countries. Ironically, efforts to combat climate change by reducing the world’s reliance on hydrocarbons could put further pressure on many resource-dependent African economies. For example, hydrocarbons account for some 35% of Nigeria’s GDP and more than 90% of its exports. Ethiopia, sub-Saharan Africa’s second-largest country, is a hot spot for recurring droughts and famines. Its population is expected to rise by 90% by 2050, from 100 million today to 190 million at mid-century. Though stories abound of “Africa rising”, the only one of Africa’s ten most populous countries that comes close to managing its population growth rate is South Africa. The other nine are all experiencing runaway population growth coupled with catastrophic economic mismanagement.

In living memory, during the era of decolonisation, Africa was a largely rural and relatively unpopulous continent. But by 2057 its population will have risen ten- fold over the 100 year history of the EU. As a result, Africa will almost certainly play a greater role in Europe’s future than it has in Europe’s recent past. Whereas the largest and most visible minority groups in Europe today originate from the Middle East, those of the mid-century will likely be of sub-Saharan origin. As a result, the EU and its member states are likely to become similar to the multi- racial societies of the Americas in their ethnic composition. Race may replace religion as the most serious fault line in European societies and politics. Border policy can shape the extent of African immigration to the EU, but it cannot prevent the shift in immigration pressure from the Middle East to Africa.

Although aid for Africa and economic engagement might help reduce future population displacements in the continent, Europeans should begin planning for a future in which race replaces religion and ethnicity as the key cultural dividing line in Europe.

EUROPE IN A WORLD OF REGIONS

The post-globalisation world has emerged as a world of three advanced, well- integrated economic regions (Europe, North America, East Asia) surrounded by countries that are connected with loose ties to these advanced regions – and hardly connected to one another at all. Europe’s eastern and southern neighbours are not connected to the European economy by the dense ties of production networks, and the stalling of economic globalisation since the Global Financial Crisis (GFC) suggests that they are likely to remain arm’s-length neighbours for some time. Europe is in many ways much more connected (economically) to North America and East Asia than to its own neighbourhood.

The halt or at least hiatus in global economic integration following the GFC is not only an external matter for the EU. Within the EU itself, trade integration has come to a standstill. It seems that the transnationalisation of global production networks has run its course. Absent any major change in the institutional environment, current levels of integration may become permanent. The EU has limited ability to shape the global institutional environment, but great flexibility to shape its internal institutional environment. An EU future that promotes greater economic integration within the Union itself could do much more than merely fulfil European Commission ambitions for an “ever closer union”. It could facilitate economic convergence among EU member states, thus providing a “free” boost to EU-wide economic growth.

The EU’s neighbourhood is largely irrelevant to this process, but trends in Eastern Europe, the Middle East and Africa will provide the context in which the EU develops over the next forty years. The EU can choose to partner with (or oppose) Russia and/or Turkey to secure its eastern borders. Whatever policy it chooses, the EU’s strategic position vis-à-vis Russia will certainly improve over the next forty years, while its position vis-à-vis Turkey will likely become more complicated due to increasing economic integration between the EU and Turkey. Any plan for Europe’s future should consider the implications for the EU’s relationships with its eastern neighbours. The implications for the EU’s easternmost countries, which must manage all aspects of the EU’s land borders (people flows, trade flows and security issues), should be given particular attention.

A dark but enduring legacy of the Second World War and its aftermath has been the relative ethnic and racial homogeneity of European countries. The Yugoslav Wars of the 1990s showed how destructive ethnic fault lines can be. Over the next forty years, it is likely that the EU will become not only more multi-ethnic and multi-religious but also more multi-racial as Europe becomes more like North America in its racial mix. At a minimum, the EU as a whole will face the kind of racialisation of ethnic relations that Italy is experiencing now, only on a much larger scale. Whether or not Europeans embrace this future, they should debate it, since the pressures that could lead to a more multi-racial Europe are almost certain to increase dramatically over the next forty years.

The European Commission’s five scenarios for 2025 (and beyond) cannot meaningfully be considered as choices in themselves. Each outlines an approach that can be taken in order to create the kinds of societies that Europeans want to live in. The actual societies that Europeans will have at the 100th anniversary of the Treaty of Rome will result from the interaction of the choices made now with larger economic and demographic forces. Any travel plan must take account of the terrain to be covered. The Commission’s five scenarios – and other possible scenarios not considered by the Commission – suggest different routes to an unknown destination. Long-term, large-scale economic and demographic trends establish the terrain that must be covered. It is for the peoples of Europe to decide what destination they want to reach, and to consider how best to get there.