News

Style Guide for Authors

more

Financial Statement of 2019

more

Available Now! Down Fell the Statue of Goliath - Hungarian Poets and Writers on the Revolution of 1956

more

Subscription

Hungarian Review annual subscriptions for six issues, including postage (choose one):

17 March 2017

Closing the Gap? The Western Community and Hungary

This is an edited version of the speech presented on 21 April 2016 at Corvinus University as part of the conference organised by Ottó Hieronymi of Webster University, Geneva, and Péter Ákos Bod of Corvinus University, Budapest, under the title “Hungary, Central Eastern Europe and the Future of the Western Community”.

INTRODUCTION: CONVERGENCE IS MORE THAN JUST ECONOMIC ARITHMETIC

Convergence of less advanced member states to some statistical average is one of the declared policies of the European Union (EU), and a significant portion of the EU budget has traditionally been spent to promote this goal since the first enlargement.1 All new member states in Central and Eastern Europe (CEE 10: Bulgaria, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Poland, Romania, Slovakia and Slovenia) are recipients of sizeable transfer flows from this budget. Net funding was as large as three to four per cent of GDP of the countries involved under the 2007 to 2013 fiscal plan, and funds of similar proportion serve the socio-economic convergence of these member states in the 2014–2020 planning period.

But convergence is much more than an issue of fund transfers, GDP growth differentials, and similar technicalities of economic growth. Catch-up with richer Western neighbours has long been a mindset of nations of this particular region. What follows is an exposition of the particular social and political importance of the hoped-for income convergence for the peoples and political classes of the region. It is quite natural to compare your wealth, income and living standards to others; families and governments as a rule mark their achievements against some chosen benchmark. The present analysis aims at explaining why catch-up to rich Western neighbours has become an overstrained driver of social behaviour and policy actions in new member states – Hungary being no exception. Perception is as important as anything in this matter: the general public’s scepticism concerning veritable convergence explains a lot of the decline in support for the EU and the West in general, in the public opinion of net recipient countries.2

It is more to it, however, than simply perception and emotion. A quarter of century of transition from the bankrupt state socialist regime to open market economy is a long enough period to provide hard facts about underlying trends and to identify particularities. Hungary, a one-time frontrunner in transition, and lately a disputed case, is unique in some respect, but being in the European periphery among a dozen similarly small and open economies, the country offers lessons of wider significance.

PATHS, TRENDS AND PERIODICAL INTERRUPTIONS

It may seem too much to go back in time to the Habsburg Empire to set the scene for the analysis of Hungary’s present socio-economic tendencies, but the historical fact that market economy (“capitalism”) emerged in Hungary during the 19th century when the Kingdom was part of a greater entity, the Habsburg Monarchy, is relevant in this context. Hungarian business life evolved in a province deprived of full national sovereignty, situated in secondary position to Vienna and the hereditary provinces of the Monarchy.

Lack of full sovereignty is a handicap, but this historical situation also involved a plus as far as Hungarian socio-economic progress is concerned: the Hungarian Kingdom was part of a sort of “common market” in the decades that followed the Great Compromise of 1867 between the Crown in Vienna and the Hungarian body politic when inter-empire trade barriers came down. The half a century between the transformation of the empire into Austro-Hungarian Monarchy and the Great War turned out to be the golden era for Hungarian capitalism, if judged by economic growth rates. Budapest emerged as an industrial, trade and administrative centre second only to Vienna. Competitive big domestic firms such as Ganz (cranes, engines, heavy industry), Weiss (from canned food to ammunition), Richter (drugs), Kühne (agricultural machinery), Törley (champagne), Pick (processed food), the state-owned MÁVAG (steam and electric locomotives), Goldberger (textile), the highly developed mills and food processing businesses supplied not just the Hungarian Kingdom but also other parts of the Monarchy, as well as markets further away. Economic development indicators (income, wealth, living standards) had placed the Hungarian Kingdom at roughly 70 per cent of those of the Empire’s core provinces by the end of this era – a significant achievement for sure.

It is still of some significance that industrialisation, urbanisation and other modernisation tendencies of Greater Hungary took place within the Monarchy which itself did not belong to the most developed part (core) of Europe in the pre-First World War period. Even the Austrian part was less advanced than Britain, Holland, Belgium and fast industrialising Germany. For the Hungarian Kingdom, being somewhat east of the centre of the Empire – on the semi-periphery, to use a modern term – was a liability in its efforts to develop. Still, its prospects of converging to the more advanced areas did not look bad at all in the pre-war years: growth rates in the Hungarian part of the Monarchy were, in spite of the complexities of the historical situation, high by global standards.

History of course then took a drastic turn in 1914. By the end of the four-year war, the Austro-Hungarian Empire had collapsed. New states were formed during the post-war crisis years – among them the now independent Hungary, a country that had to cede two thirds of its historical territory to other new entities (Czechoslovakia, Yugoslavia and Greater Romania). A sovereign Hungarian state and a viable national economy had to be created in a period of revolutions and occupation, incidents of lawlessness and tensions with the newly created neighbours. On top of that, the global crisis of 1929–1933 then took its toll.

In spite of all these shocks, independent Hungary – much smaller and now land- locked – managed to recover from the post-war chaos. The economy was able to efficiently absorb foreign loans and direct investments. Many domestic firms such as Tungsram (light bulbs), Orion (radio), Rába (trucks), Ganz-Danubius (shipbuilding) emerged as major players in European markets. Hungarian technical development level and educational standards were high, research capacities in certain sectors were up to global standards. The Nobel Prizes of Zsigmondy (chemistry, 1925), Szent-Györgyi (medicine, for vitamin C, 1937) and Hevesy (chemistry, 1943) are indicative of the intellectual advancement of Hungarian academia and research in the interwar years. Technical geniuses, most famously Szilárd, Teller, Wigner and Neumann – scientists of Hungarian origin who, due to the sinister political tendencies of the era, had to leave their home, went to work with Fermi and Einstein on the Manhattan Project (that produced the first nuclear weapons) during the Second World War, owed a lot to excellent Hungarian schools.

It is a justified claim that at that particular period Hungarian intellectual, academic, technical and business standards were probably the closest they ever got in history to those of core countries, the present times included. One may also call exemplary how much investment went into what we now call human capital through the development of public education, from elementary schooling to higher education, or of public health leading to the eradication of tuberculosis. This claim about the achievements of interwar decades does not aim to whitewash the political regimes of that era but to shed some light on the real standing of contemporary Hungary vis-à-vis its neighbours and its natural comparators, in the last period of capitalism before the long detour starting after 1945.

Foreign trade links, quite naturally, tied landlocked Hungary to Western and Central Europe in the interwar period. Unfortunately, through exports, the country soon became over-dependent on German orders even before the outbreak of the Second World War – one of the many components of a deadly alliance with Hitler’s Germany.

Hungary suffered terrible human losses, military occupations, damages to the economy and the loss of sovereignty during the war years. Then, as a satellite country under the close political, ideological, military and economic control of the USSR after 1945, Hungary was soon cut off from the West. The geographical orientation of foreign trade and finance changed drastically as the Soviets forced their interstate barter settlements called Council of Mutual Economic Assistance (CMEA or COMECON) on their allies, the People’s Republic of Hungary included. Within CMEA the USSR became the major trading partner. This led to Hungary having a distorted industrial structure that was not compatible with its factor endowments, technical traditions, and potential competitive advantages.

Forced industrialisation and urbanisation, as customary in certain periphery and semi-periphery countries, initially resulted in high economic growth figures. But state dominance, one-party political rule, anti-market ideology and stunted links with the West (seen as a potential lethal enemy) disfigured the technical, economic, scientific and intellectual structures that determine the level of advancement and the sustainable qualities of a socio-economic system. The sad consequences revealed themselves in full only once the regime disintegrated four decades later all over the CEE region, and the artificial trade structure collapsed.

Still, the Hungarian version of a Soviet-type system retained some specific features. Orthodox Communist rule, to start with, lasted shorter in Hungary than in some other peers under Moscow’s command as the result of the October 1956 Revolution. The Hungarian Revolution and anti-Soviet freedom fight was crushed brutally but the post-1956 Communist regime could not restore the status quo ante. Economic reforms were introduced in the 1960s. The softening of the rigid socio-economic system was not uninterrupted in the decades that followed, but the People’s Republic of Hungary came to an end in 1989 in much different conditions than those countries of the region (e.g. Romania, Bulgaria, Czechoslovakia, East Germany, and the Soviet Union itself) that had not experienced a similar heterodoxy during their four – or in the case of Russia seven – decades of command economy.

Communist rule suddenly ended in the Annus Mirabilis of 1989. Yet, it was clear for the informed that the return to a market economy, parliamentary democracy and to the Western community would be far from smooth in Eastern Europe. The longer the hiatus, the harder the return to a market based economy would be. It stood to reason that Czechoslovakia, Hungary, Poland (countries that formed the Visegrád 3 regional grouping in 1991) stood a much better chance than Russia or Ukraine to get over the transition period and to become market economies again. Yugoslavia then became immersed in bloody separation conflicts, one result of which was the Balkan countries mired in much worse shape economically and politically than the Visegrád (V3) set. Still, no one could properly foresee the depths of the economic contraction and the complexities of social transformation that transpired right after the long-awaited political changes even in the V3, later to become V4 after the break-up of Czechoslovakia in 1992–1993.

THE NEW WORLD IN 1990

Political transition was coupled with a deep decline of output, jobs and income even in the more advanced former planned economies. This came as a nasty surprise. The expectation had been, and not only among the naïve masses but also in think-tanks and international financial institutions that the reform-socialist past of Hungary, Yugoslavia and Poland would be an asset, and the lack of it elsewhere a handicap. Yet, the Schumpeterian “creative destruction” took its toll all over the region. Hungary’s GDP declined in three consecutive years by about 18 per cent altogether, in Czechoslovakia by the same, in Poland a bit less – but there the decline started much earlier and the rock bottom had been reached already before 1990. Other nations suffered even deeper contraction, including East Germany whose industry collapsed übernacht after unification.

The shocking size of contraction made clear that the state-centred old system had been much less competitive economically than both its proponents and its critics had once claimed. Steep decline in output and employment said a lot about the rotten shape of former planned economies, whether orthodox or reformed types. In addition, the nature of the world economy and market order that these nations joined in 1989–1990 was fundamentally different from the one they had been once part of in the 1930s, never mind the pre-First World War era.

First, by 1990, markets had truly become global at the time when CEE national economies opened up fully to flows of goods, funds and information. Second, at that historic moment, major economies happened to be run by free-market governments, like those of Ronald Reagan and Margaret Thatcher. International financial institutions (IFIs), particularly the International Monetary Fund and the World Bank, advocated liberalised trade regimes and swift privatisations in post-Communist countries. Policy advice that the democratically elected new governments received from IFIs, friendly governments and most of the academia was predominantly neo-liberal in its general attitude to economic change.3 To put simply: the world economy had changed beyond recognition by 1990.

Knowledge of how to run a national economy in a democracy was obviously scarce in post-Communist societies. Moreover, whatever administrative skills and economic knowledge the emerging new political class possessed was summarily declared outdated by the champions of the free-market era. The 1990s was a decade of glorious globalisation, with an American accent in business practice, macroeconomics and social policies.

Was Western European capitalism different? What about Germany? This is a country that had accomplished a profound regime change four decades earlier, following the collapse of the National Socialist rule. West Germany, as decision- makers in the new Hungarian government in 1990 recalled frequently, emerged energetically from the post-war abyss and was thus seen as a success story. It was also known in professional circles that the West German government applied the heterodox recommendations of the so-called Freiburger Schule in those successful decades: Ordnungspolitik built on the theoretical body of Ordoliberalism. The German version of market economy with its emphasis on open markets, freedom of contract, strong antitrust policy, participation of employees and employers in decision making, support to small and medium enterprises, proved to be up to the transformation challenges that Germany met in the 1950s. The German-type social market economy thus served as a model for the emerging Republic of Hungary – see the reference to social market economy in the Preamble of the 1989 Constitution of the Republic of Hungary.

Still, a similar Hungarian effort to rebuild market order on the model of a social market economy did not have much external support. Not even from Europe. This caused certain disappointment for the first democratically elected government, but it is less surprising with the benefit of hindsight: post-war reconstruction had become ancient history by 1990 and it was the promises of globalisation that instead sounded convincing. By 1990, Western Europe had already gotten over the shocks of the first and second oil crises. Some European nations embarked at that historic moment on downsizing their welfare state in order to regain a competitive edge, and all embraced globalisation. This remained thus the sole model for the transition nations – whatever their conditions and expectations.

Incidentally, right at the historic moment when the Berlin Wall came down, European integration also entered a new (and risky) phase of creating a common currency, the euro as it was named later. A common currency presupposes profound harmonisation of institutions, policies and economic structures. That is, it is about deepening, rather than enlarging. The EEC 12 (six founding states and six newer members) had just completed, after decades of gradual harmonisation efforts, full current and capital account liberalisation by 1988 – the very year when opposition parties in some Communist-ruled countries started to emerge in anticipation of systemic changes that might take place in the not-too-distant future. Now we all know that Big Power positions changed faster than anticipated, and civic opposition to the corrupt, sclerotic or oppressive regimes gained momentum surprisingly fast. In a year or two, a set of countries knocked on the door of Europe which itself happened to be preoccupied with the tasks of adding monetary content to common market structure.

INCOME CONVERGENCE AND/OR NATION-BUILDING

Given the particular historical antecedents, it is not surprising that in 1990 many Hungarians saw their future, if not immediately then soon, as becoming citizens of a free and well-off society, somewhat resembling neighbouring Austria. We know that this was and still remains a misplaced comparison. Austria was already much richer than the EU average before joining the Union, and Austrian per capita GDP in 1991 exceeded 135 per cent of the EU average.4 For comparison: the same mark for Hungary was only about 50 per cent. Others in the region did not fare better, with the exception of the Czechs and Slovenes who stood at about 60 per cent. Slovakia stood at 40, Poland at 30 per cent. Austria has been doing better economically than the rest of Europe ever since: 7th highest place in Europe in terms of the GDP per capita, surpassing Germany (9th) or Great Britain (15th) according to 2014 data.

Well, as noted earlier, it was a long time ago when Hungary’s national income level reached 70 per cent of Austria. The latter became an advanced welfare state after the Second World War, supported by a diversified economic structure with steel and manufacturing to agribusiness, to summer and winter tourism, to strong banking and insurance. In contrast, during the same period, Hungary, and the rest of the region, was subjected to a forced industrialisation experiment between the 1950s and the 1980s which left behind at the time of the regime change an oversized industrial sector, underdeveloped physical and financial infrastructure, and unmet demand for quality consumer and industrial goods.

The very first years of transformation could not be but drastic for the societies concerned. Unemployment suddenly exploded: loss of jobs was, at first, caused by the unavoidable transition crisis. Later, it was due to skill-biased economic modernisation: domestic and foreign private firms absorbed young, healthy and trained labour, but shunned the old, the less mobile, and those without language and computer skills. The collapse of the whole inter-governmental barter regime of CMEA was unavoidable and foreseen, but the fact remained that certain large scale industries were washed away as a consequence. The underdeveloped service sectors, on the other hand, started to grow dynamically: telecom, retail, banking, insurance and logistics experienced unprecedented expansion. But with limited domestic capital stock and market skills, the mentioned sectors have been easily penetrated by foreign firms (Austrian, German, Italian, American first of all). These nations were also overrepresented among buyers of state owned enterprises that were put up for privatisation.

After the first couple of crisis years, all transition economies started to grow, first at a slower pace. In the second half of the 1990s and particularly after year 2000, growth data looked impressive. A higher than EU average growth rate in the CEE region meant that at last real convergence was taking place. On the face of it, the first two decades of transition of the V4 have been successful.

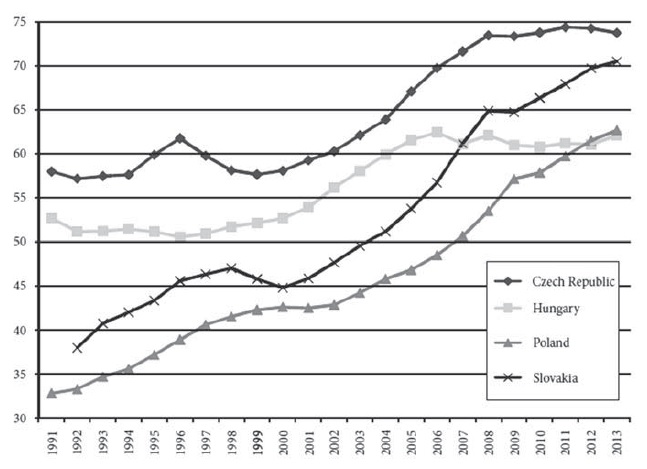

Economic convergence in the Visegrád countries, based on GDP per capita, at purchasing power parity, as percentage of EU15 average. Source: Oblath, 20145

A message of the chart is that, in spite of what many feel, there has been considerable convergence to the European level: the V4 countries’ relative range in the early 1990s was 35 to 60 per cent of the then average, while the recent range is 60 to 75 per cent. Second, Slovakia and Poland have accomplished a remarkable convergence performance, compared to the Czech and particularly the Hungarian case. Third, convergence has not been continuous: in the two latter cases no convergence to the core has taken place since 2008 (Czech Republic) or even since 2005 (Hungary), and leaves the nations still far from their long-term, historic relative positions.

Some other former planned economies have accomplished a truly spectacular performance in their catch-up, having started from a lower level (Estonia, Latvia, Lithuania, and more recently Romania).

The general picture of the post-Communist countries, thus, looks positive, particularly against the controversial story of the other periphery regions of Europe: the Irish catch-up has been impressive, the Spanish, Portuguese case is debatable, while Greece has not been able to get closer to the core in terms of GDP level. These economies, with the notable exception of Ireland, having spent four to five decades in the EU have mostly remained in the 70 to 90 per cent range.

At first glance, CEE nations should be satisfied with their relative performance, and with the key institution, that is the EU, of their growth framework. But European polls report that societies mostly feel otherwise. Hungarian evaluation of the state of the national economy is predominantly dire (27 per cent positive, 72 per cent negative, the rest is undecided), against the European average (39 per cent P, 57 per cent N) under the 2016 spring survey of the Eurobarometer. As for the general view on the EU, the EU28 results are slightly in favour (34 per cent positive, 38 per cent neutral, 27 per cent negative). The corresponding figures for Hungary are 33, 41, 25; similarly slightly supportive of the EU, but less than appears logical given the strong net money inflows. The Polish data reflect strong support, Slovakia is lukewarm, and the Czechs are predominantly EU-sceptic with 26, 40, 34 per cent, respectively.

There is no room here to analyse the motives and objective factors behind the negative-neutral public evaluation of a nation’s situation, but certain components should be mentioned. One is the particular modalities of the regime change in 1990 and the road to EU accession (2004 in most cases).

As already indicated, transition from the old regime to a market-based system took place at a time when globalisation was the only game in town. Former planned economies that happened to be in different and diverse macroeconomic situations themselves and were at different level of readiness for social changes, suddenly were exposed to a full market opening in the early 1990s. They were also advised to deregulate the economy immediately, and privatise the oversized state sector at full speed. It is worth recalling that while Western Europe and its semi-periphery had gradually carried out similar policy reforms over a course of decades, the newcomers on the other hand were encouraged to see fundamental reforms through in a very short space of time.

Market opening, deregulation (that is, the decrease of the regulatory role of the state), and privatisation did accelerate the structural transformation of the economies in case, but also enabled the swift market penetration of foreign business. As a result, transition economies quickly became extremely open to trade and financial flows. At the time they entered the EU, foreign trade volumes of goods and services were as high as in the most open economies of the EU (Ireland, the Netherlands) – but the latter had been given several decades to open up their economic sectors, and to prepare the general public for the consequences of full openness.

Older European member states are also open economies with huge export and import volumes, but against their statistics, the foreign trade openness of Slovakia, Hungary, Estonia, and the Czech Republic looks outstanding. Net exports have become a key driver of CEE growth.

Still, high openness involves risk factors: extreme exposure to the global business cycle, and concomitant demand volatility. Also, if sensitive business decisions are taken elsewhere, in foreign headquarters that is, such a dependency may cause uncertainty and political tension within the country.

In all these cases, high trade openness goes together with high share of foreigners in the capital stock of the economy. Capital income gained by foreign factor owners bloat GDP figures but such incomes do not belong to domestic agents (residents). Therefore GDP level and growth data tend to over-report the real income situation of the country in case.

A sector that has been the target of penetrating foreign capital in CEE countries is banking. Although particular country cases differ, foreign banking dominance became customary in the region after the first decade. This should not come as a surprise since planned economies back in the 1960s and after became middle income nations with an oversized industry and underdeveloped service sectors – and this historical legacy had its lasting impact on the structure of their market economy system. Thus entry of foreign capital is a logical consequence of previous negligence of the service sector, particularly of banking, under the centrally planned regime. Still it is noteworthy that this region is exceptional globally as far as the high share of foreign owners in domestic banking (and insurance) is concerned. In most other parts of the world, whether developed or less advanced, majority of ownership tends to belong to domestic actors, due to the general effect of “home bias”, so characteristic of financial services.

Even after decades of transition, former planned economies are still under-banked: the stock of banking assets is equal to one or one-and-half of annual GDP, a crude measure of financial depth, while countries in the “other periphery” have twice as high a ratio.6 And one more difference: while in Spain, Italy, Greece, Portugal most banks are owned domestically, the financial sector of certain transition economies (Czech, Croatian, Estonian, Slovak, Romanian) are practically fully foreign owned.

Interestingly enough, the country where regaining majority national control over banks became a strategic policy goal, Hungary, had already a rather balanced ownership structure by the time when the declaration about controlling at least half of the banking sector was made by PM Orbán. His government adopted policies to increase the tax burden on banks. That led to heavy losses in the financial sector and made some banks consider abandoning the Hungarian market altogether. Without discussing here the overall balance of this policy line, one can see that efforts to regain national control of the banking sector as a key industry do not come free of charge. First, renationalisation incurs costs on the budget. Second, and more importantly, the mere fact that a government renationalises foreign-owned financial institutions or supports privileged domestic businesses to buy out foreign owners, might create a business atmosphere that can restrain the capacity and willingness of banks to take long-term risks. There exists thus a potential for “patriotic policy versus economic growth” trade-off. Pursuing the first goal works against the other, equally much wanted, goal: high economic growth rate. You cannot have both at the same time. Hungary’s lack of real convergence in the 2005–2016 period is partly due to the fact that government policies have caused significant growth rate sacrifice. Such trade-offs do not easily enter the political calculations of decision- makers who pursue policies to strengthen national sovereignty.

Nation-building is not something that only occurs in the developing world. New nation states emerged around 1990 as a consequence of disintegration of former entities (USSR, Czechoslovakia, Yugoslavia) – some peacefully, others less so.

The limited number of country cases makes generalisation difficult but one can still posit that some societies and their ruling elites that faced nation-building tasks put extra efforts into structural reforms, including meeting entry conditions to the eurozone, as in the case of Slovenia, Slovakia and the three Baltic countries. This is in contrast with Hungary or Poland where adoption of the common European currency or winning the status of “international excellence in the class of new member states” has not become an overarching, unifying national theme, and euro-adoption has remained mostly a technical issue.

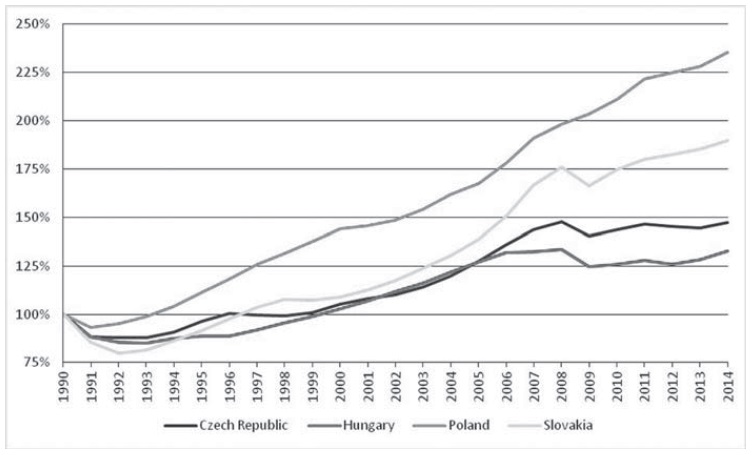

Economic growth rates over a quarter of century do provide valuable inputs into understanding the significantly different performances of transition countries, even if GDP data are not perfect indicators of socio-economic progress. Yet, a glance at Chart 2 helps us visualise the various phases of the profound transformation of these countries.

Growth of real GDP: some are more successful than others. Source: UN National Accounts Main Aggregates Database. Prepared by András O. Németh, Corvinus University.

The first period (1990 to 1997/1999) – which lasted surprisingly long, with the exception of Poland – was the recovery of output to the pre-transition level. The second period after that until the global crisis is the one that seemed to deliver, somewhat belatedly, what had been promised to the peoples of the region: economic growth, increasing living standards, acceptance into the core Western institutions (OECD, NATO, EU). But that growth trend ended in 2008, and the latent divergences among countries have become more pronounced since then.

This is the state of affairs a quarter century after the political regime change in the region. Surpassing the very modest output level of 1989 by 30 to 50 per cent 25 years later – as is the case with Hungary and the Czech Republic – is not something to be proud of. The Slovak case is stronger, and even more convincing is what has taken place in Poland. But on the whole, the transformation story is far from a Wirtschaftswunder – and large parts of the societies concerned feel disenchanted or even betrayed.

Would the above facts, trends, and perceptions justify the questioning, let alone the rejection of Western values? Is it the market economy model as such that has proved to be less than successful? My answer is no on both accounts. To start with the second: the efficiency of market-intermediated exchange is conditional on the legal, institutional and political framework, as well as on knowledge, skills and values of the society. These preconditions are still not fully met in periphery and semi-periphery societies. The catch is that when they are lacking, the efficiency of the market system – particularly when exposed to the tough competitive pressures of a global order – will obviously lag behind both that of the model economy in abstracto and that of the actually existing benchmarks of Western economies. To put it simply: periphery capitalism is seldom appealing.

And that takes us back to the first issue. Less than hoped-for results feed into criticism of Western values, and strengthen the voices of those who advocate other models – even if the mere applicability in CEE, not to mention superiority, of oriental command economy or illiberal regimes cannot be justified by theory or practical examples.

But such feelings and perceptions are around, and they have to be taken into account when one tries to map future paths of this fast-changing and thus somewhat unstable region. What concludes this essay is therefore the overview of tendencies and risk factors that may have determining effects on the future progress of the region, and its relations towards the Western community.

THE HUMAN FACTOR, THE NEXT INDUSTRIAL REVOLUTION AND OUTLOOK

Given these facts and trends surveyed, the present mixed state of affairs of the CEE countries seems to be less surprising. What bothers many analysts and commentators is the lukewarm support for the liberal market order and the European norms in transition countries – or in the “second semi-periphery” of Europe.

Well, hard economic data and polls on subjective factors provide abundant explaining factors that help us understand the case. The region was, from the very start of the transformation process, exposed to a “shock therapy”, whether that was government policy, like in Poland in 1989/1990, or not, like in the case of Hungary under the first freely elected government of PM Antall. But even in the latter case, with strong professional and societal arguments for gradualism, economic transformation actually took a radical way. Transition shocks were enlarged by the extreme contrast between the actual state of the transition countries on the one side, and the rules and requirements of the globalised world economy, on the other. This contradiction resulted in an unplanned destruction of a serious part of the physical and human capital stocks of the nations concerned. Policy advice from the Western community was also pushing decision makers to adopt practices that led to shock-like consequences in the first decade. Across the region, modernisation was fast but hardly organic, nor universal in the first period of transformation. This time, it was not the case of forced industrialisation à la Soviet, but industrial change was certainly faster than the adaptive capacity of a significant part of society. Such capacity turned out to be very much age- and skill-dependent: the young and the educated internalised the values and norms much faster than others. The spread of the modern market economy structures turned out to be uneven also in regional aspects: faster in the capital city and in the western part of the countries, and rather protracted in rural areas.

In the second phase, from the late 1990s up to 2008, the original growth model built on the marriage of cheap local labour and foreign direct investment (FDI) eventually delivered its results, but gradually approached its limits in the more advanced transition cases. The results were real, not imagined. Brand new industries appeared in the region: automotive assembly and components (“Detroit East”), consumer electronics and parts, business services. Firms, foreign and to a lesser degree local, managed to capitalise on labour supply and government incentives, and took advantages of good location. Real wages started to grow, consumer choice and service level in the privately owned sectors (telecom, banking, retail) increased impressively. But the spread of advanced technology and concomitant higher productivity was slow and restricted regionally and sector- wise. All concerned countries are characterised now by having a dual economy: an advanced and productive large-scale and mostly foreign owned sector, and a second, less productive, low wage, undercapitalised domestic sector that happens to employ the majority of the labour force. Such a duality unavoidably causes societal and political tensions.

The 2008 crisis exposed the vulnerability of the FDI-driven model, and delivered the trade-dependent “second semi-periphery” a heavy blow when international flow of funds suddenly stopped. Since then, financial and trade flows have returned to normalcy, and net export has become a growth driver of the CEE countries – but the crisis has left its marks on society.

The social reaction to the 2008 crisis included the re-emergence of national solutions to problems, with non-conventional policies such as nationalisation, reindustrialisation programmes, protectionist and selective tax measures – with mixed results, like in the case of Hungary.7 Some other countries with reserve labour to be used seem to keep benefiting from FDI inflows in search for higher yields (Slovakia, Romania) and have managed to maintain high growth rates until very recently.

But the original growth model is losing relevance all over the region, even among the latecomers, outside the V4. Abundance of well-trained and inexpensive labour was the case two decades ago but it does not hold anymore, partly for demographic reasons. Birth rate is low or even lower in the CEE and SEE region than the European average. What is more, there has been a steady outflow of migrant labour from the region to Western Europe. The size of the depletion of the stock of employable labour due to emigration varies a lot by countries, ranging from over 10 per cent in Romania and Latvia to five to six per cent in Bulgaria and Poland to three per cent in Hungary and less in the Czech Republic.8

The migration trend points steadily upward and countries with still moderate emigration may experience accelerated outflow. It is telling that the 2016 labour reviews in Hungary reported a very serious (quality) labour shortage in a range of professions from doctors to shop assistants to IT specialists – jobseekers can find employment in high wage Western countries.

Mass migration is driven by real and perceived wage differentials. The region has been known as a low wage cost area for decades. Industry wage differences between Austria and Hungary or between Germany and Poland are at present about 4:1, between Sweden and the Baltic countries they are even higher. It is not surprising that mobile labour has found its way from a low-wage region to Western and Northern Europe.

But these discrepancies have existed for a long time; so why is migration so much higher now? One obvious factor is the eventual removal of labour movement restrictions that certain EU member states retained legally after the 2004 enlargement. The seven-year maximum restriction period expired in 2011, leading to a jump in legal migration into Germany and Austria (the UK, Sweden and Ireland did not apply temporary restrictions when CEE countries became members in May 2004). The other factor is the perception as catalyst for change: a decade of full membership in the EU was enough for the citizens of the new member states to get accustomed to being equal to the older (and better-off) members. But formal equality does not go together, obviously, with having a similar income level. The income gap may have been somewhat reduced between old and new members in the last dozen years, but the remaining differences in living standards and wages in CEE vis-à-vis richer neighbours have become more irritating. This is particularly true for the new generation that customarily compares cross-border conditions.

Would accelerated real wage increase in the CEE region be enough to slow down and eventually stop emigration? Hardly. Wage differences do not disappear for decades. Income convergence and improvement in work conditions may appear relatively fast from an economic history perspective but less so by the younger generation. As a consequence, a declining labour supply in the CEE region is a very real tendency, exacerbating the contradictions of the present growth model. This model will be increasingly undermined by the technological and organisational advancements that are commonly referred to as Industry 4.0. The widespread use of robots and algorithms would soon reduce demand for repetitive and simple jobs in service and industry, that is in the very classes of employment that CEE nations had excelled in during the first decade right after the region’s reintegration into the global supply chain. While the spread of new technologies is a welcome event in CEE, many existing jobs are endangered in the process, and training the youth for soon-extinct jobs is pointless.

Another logical tendency which still carries risks for the existing socio-economic model is the probable decrease in the size of EU fund transfer to the region. Net funding has been a major growth driver, particularly in the case of Hungary where net EU inflows in the 2013–2015 period were as high as five to six per cent of GDP. The beneficial effects of such sizeable transfers are hard to overestimate: EU funding helped reduce the external financial exposure of the country, and added to the aggregate demand. It is still noteworthy that in spite of the huge size of the inflows, Hungarian growth rates remained moderate by EU-periphery norms, and the competitiveness ranking of the country has not improved at all. Still, a probable significant decrease of the volume and proportions of net EU funding in the post-2020 period would again cause a sort of negative shock.

Protectionism, always coming to the fore in times of troubles, would be a short- sighted, dangerous and self-defeating policy reaction for countries so open to global processes. Support for the weak and concentration of resources through the state may sound appealing but could degenerate into cronyism and favouritism – the very enemies of market efficiency and democratic order.

Obviously the old formula will not work better over time, if not for any other reason but the lack of cheap, well-trained labour eager to accept slightly higher pay and somewhat better job conditions than before. A new development model is thus needed for the region as a whole, and particularly for the Hungarian economy with its modest growth capacity. Hungary is not without supportive structures and potential allies though, in its search for a new mode of operation. For such an extremely open economy, so dependent on European markets, existence of harmonised EU-wide framework conditions is vital. Remaining within the so- called Schengen area is a must, given the high degree of integration of Hungarian firms into Western European chains. A hoped-for technological upgrading of the industrial activity, and more high value-added service activities would not necessarily increase the volume of product flows between Hungary and its main partners; still, no interruption of flows remains a key precondition. Proximity of growth poles within the otherwise moderately dynamic European economic area remains a major asset.

Economic growth, however, will not in itself solve the socio-economic tensions generated by the slowness of the catch-up process. Periphery countries, it has become obvious, need flexible local social protective institutions, but at the same time they must prepare for Industry 4.0. This is a unique challenge, for the whole CEE region, comparable to those that have been surveyed above.

REFERENCES

Bod, Péter Ákos (2015): “Economy: Non-Conventional Measures”. In John O’Sullivan, Kálmán Pócza (eds.): The Second Term of Viktor Orbán: Beyond Prejudice and Enthusiasm. London: Social Affairs Unit, 2015. pp. 131–146.

Forgó, Balázs and Anton Jevčák: Convergence of Central and Eastern European EU Member States over the Last Decade (2004–2014). EC Discussion Paper 001, 2015, ec.europa.eu/economy_finance/ publications/eedp/.../dp001_en.pdf.

Hieronymi, Otto (ed.): Hungarian Economic, Financial and Monetary Policies: Proposals for a Coherent Approach. Battelle Europe, 1990.

NOTES:

1 The single biggest item in the seven-year financial framework 2007–2013 as well as financial framework 2014–2020 is Item 1b named Cohesion for Growth and Development and Economic, Social and Territorial Cohesion inc. regional convergence. See: http://ec.europa.eu/budget/figures/ fin_fwk0713/fwk0713_en.cfm#cf07_13.

3 Let us mention among the notable exceptions the Report of the Battelle Memorial Institute under the leadership of Otto Hieronymi (Hungarian Economic, Financial and Monetary Policies: Proposals for a Coherent Approach).

4 Monthly Report, January 2016. http:// www.ac.at. Publications: www.monthlyreports.

5 Oblath, Gábor: “Gazdasági instabilitás és regionális lemaradás. Magyarország esete” [Economic instability and regional backwardness.The Hungarian case]. Külgazdaság, Vol. 58, Nos. 5–6, 2014.

6 See: Forgó and Levcak, 2015.

7 See my analysis of the 2010–2014 period: Bod, 2015.

8 2013 estimation by Eurostat EU LFS.

You have to log in or registrate for writing comments.